Weekly Brief: Credit

Even the Equity Is Mostly Debt

By Davide Scigliuzzo

At first glance, the financing for Apollo Global Management Inc.’s acquisition of a suburban phone and internet provider looks like a textbook leveraged buyout: one part equity, two parts debt.

But look a little closer and you’ll notice something odd: most of the equity check is debt financed as well. The high leverage levels on this buyout help explain why banks were forced to pull their sale of bonds and loans tied to the deal.

Over 60% of the $3 billion equity commitment that Apollo has agreed to pay to acquire telecom and broadband assets from Lumen Technologies Inc. -- which will be run under the Brightspeed brand -- will come from a five-year loan provided by banks, according to a person familiar and debt documents reviewed by Bloomberg.

The $1.9 billion loan is separate from the $6.3 billion of debt that Apollo also plans to use to finance the acquisition. Selling even a portion of that debt has been hard: Groups of banks led by Barclays and Bank of America shelved a $3.9 billion offering of bonds and loans on Sept. 29, after finding relatively few buyers.

The banks underwrote the debt commitment for the LBO. That means they would be on the hook to provide the cash themselves and retain the risk on their balance sheets. The buyout is expected to close on Oct. 3, according to a filing.

The loan for Apollo’s equity is issued by a holding company that benefits from no guarantees or security from Brightspeed’s operating assets. And it is Apollo, rather than Brightspeed, that’s expected to pay the principal and interest, according to reports from credit-rating firms.

It’s an example of the many types of backleverage -- or debt that’s incurred on an equity investment -- that have become increasingly popular among private equity firms. The arrangements, which can be specific to an individual investment or apply to entire funds or portfolios, can be used to boost returns, increase liquidity or monetize equity stakes.

But it’s also a symptom of frothy debt markets, exactly the sort of thing the Federal Reserve is looking to rein in as it hikes rates and tries to tame inflation.

Because the banks providing the financing for the equity commitment have a claim on that equity, the facility charges a much lower interest rate than what the telecom company is expected to pay on its own debt, said the person, who asked not to be named when discussing confidential deal terms.

Representatives for Apollo and Brightspeed declined to comment, while Lumen didn’t respond to requests seeking comment.

Relying on borrowed funds rather than drawing the entire $3 billion from its investors will allow Apollo to provide Brightspeed with much-needed cash to upgrade its network to fiber optic cable while limiting the negative effect that such a large outlay would have on the fund’s internal rate of return -- a closely watched measure of performance for private equity investments. Brightspeed is expected to have nearly $1.5 billion of cash at closing, according to the deal documents.

The $6.3 billion of debt that will be layered onto Brightspeed’s balance sheet includes $2 billion of leveraged loans the banks tried to sell, $1.865 billion of bonds they sought to sell, both of which were pulled, plus a $1 billion term loan that banks will keep on their books, and $1.4 billion of existing notes that will remain in place.

A drop in risk appetite among investors has already forced Wall Street banks to offload chunks of debt for the buyout of Citrix Systems Inc., which is expected to close this week, at steep discounts, and to keep nearly half of it on their books.

Complicating matters further, some holders of the bonds that are expected to remain outstanding as part of Apollo’s Brightspeed acquisition have claimed that the new financing would put one of the company’s subsidiaries in default by violating terms of the existing debt agreements, Bloomberg has reported.

Apollo has the option to delay interest payments on the five year loan through a “pay in kind” feature, the debt documents show. The private equity firm can voluntarily repay the loan at a premium during the first year, and with no premium or penalty thereafter.

S&P Global Ratings points out there are few restrictions on Apollo’s ability to upstream cash from the operating company to the holding company to repay the loan.

— With assistance from Paula Seligson

UK and European high-grade corporate bond spreads blew out to their widest levels since the early part of the pandemic, after the UK's Chancellor of the Exchequer proposed a budget that would cut taxes for the wealthy by the most in 50 years, funding it with more borrowing. (See Datawatch). The nation's bonds tanked, as did the pound, bringing corporate bonds along with them. A Bank of England intervention helped shore up markets, but still left them damaged. European debt was also hit by concerns about the region's natural gas supply, after Russian energy firm Gazprom warned that two gas pipelines might have been deliberately damaged. Even US investment-grade corporate bonds weakened, with spreads reaching their widest since July. US junk bonds fell to their weakest levels since mid 2020.

The cost of insuring against European company debt against default in the credit default swap market surpassed peaks hit during the pandemic this week, and touched levels last seen during the 2012 euro debt crisis. The iTraxx Europe index of investment-grade credit default swaps topped 142 basis points at one point on Sept. 28 to hit its highest level since September 2012, when the euro area was reeling from a debt crisis, before settling down to close at around 135 bps. An indicator of junk-rated debt approached a similar milestone.

Suncor Energy is pushing ahead with a bond buyback as oil prices near this year’s lows amid recession worries. Calgary-based Suncor plans to buy up to C$1.75 billion ($1.27 billion) of securities from 10 series of outstanding notes in US and Canadian dollars, the company said in a statement Monday. Cenovus Energy, another large Canadian oil company, did a similar offer earlier this month.

The Treasury Department is coming up with guidance for the 15% minimum tax on domestic companies, and Congressional Democrats are urging the department to ignore appeals by lobbyists to weaken the law. Senators Elizabeth Warren, Angus King, Michael Bennett, and Representative Don Beyer, asked Treasury Secretary Janet Yellen and her staff to take an aggressive stance against companies that seek carve-outs or other modifications to the minimum levy. The tax takes effect in 2023, and Treasury has yet to issue guidance on it, although officials have said it's a priority in the coming months.

The Federal Reserve Bank of New York's Corporate Bond Market Distress index showed rising stress in December. The measure, based on a 0 to 1 scale, with 1 showing the highest stress, rose to 0.28 on the week ended Sept. 23 from 0.24 in late August. It is now just shy of late July's 0.29 and close to Nov. 2020 levels.

Hedge funds including Saba Capital are lobbying advisers of UK cinema operator Vue International to publicly disclose details of a debt restructuring so that they can reap a payout on credit derivatives linked to the company. The problem lies with credit-default swaps. In order to get paid, information about the underlying debt must be publicly available. In the case of Vue a restructuring deal approved by lenders last month could keep the underlying loan terms private, putting the payout at risk for holders such as Boaz Weinstein’s fund. The funds are now pressing the company, advisers, trustee and agent of the loan to make the documents available, according to people familiar.

Bond issuers are asking banks to help them win investor permission to convert old debt into a fast-growing and sometimes controversial type of ESG product. The goal is to turn regular bonds into so-called sustainability-linked bonds. SLBs tie interest payments to a company’s environmental, social or governance performance, and come with triggers that give them meaningfully different profiles from conventional bonds.

The pile of distressed US dollar-denominated debt outstanding rose by about $10 billion last week, reversing a contraction from the previous week, according to data compiled by Bloomberg. The heap of corporate bonds and loans in the Americas trading at distressed levels swelled to $196.7 billion late last week, about a 5.4% increase from $186.5 billion a week earlier, according to data compiled by Bloomberg.

Banks pulled bond and loan sales tied to the Brightspeed LBO. A group led by Barclays shelved a roughly $1.9 billion junk-bond sale on Sept. 29, while a group led by Bank of America pulled a $2 billion loan sale. The Wall Street firms struggled to attract demand from investors for the debt, which is helping to finance the buyout by Apollo Global Management Inc.

The banks underwrote the debt commitment, meaning they would be on the hook to provide the cash themselves and retain the risk on their balance sheets. The LBO deal is expected to close on Oct. 3, according to a filing.

There were no other deals in the US junk bond primary market. Yields have climbed to a two-year high across all high-yield ratings as risk averse investors pull cash from junk bond funds.

The week’s other big story was Saudi Arabia’s sovereign wealth fund mandating banks for a dollar green bond sale as the kingdom seeks to reshape its reputation on environmental issues.

The PIF, as the fund is known, is working with lenders BNP Paribas, Citigroup, Deutsche Bank, Goldman Sachs and JPMorgan on the debut multi-tranche ethical sale, the same people said. Investor calls for the offering started on Tuesday and books may open as soon as this week.

US investment-grade bond sales fell off this week as volatility stemming from the Federal Reserve’s recent rate hike and a crash in the British Pound. Just two companies sold debt early this week, while most borrowers that had been looking to sell debt stood down, dealers said.

Atmos Energy, a utility, and captive finance company Paccar Financial were the sole issuers. Both are considered “defensive credits,” which are typically the first to come back into the market following bouts of volatility. Issuers paid 15 basis points in new issue concessions on order books that were 2.7 times oversubscribed. Sales this week stand at just $1.1 billion, well short of estimates calling for $10 billion to $15 billion of issuance.

Early estimates from dealers suggest September sales for US investment-grade may total about $75 billion. Forecasts have missed estimates three of the past four weeks, suggesting that it’s tough to call.

Issuance in Europe’s primary market slowed markedly this week as gauges of risk spiked above peaks seen during the coronavirus pandemic and touched levels last seen during the 2012 euro debt crisis. Sentiment deteriorated as investors weighed up threats including energy supply disruptions over the winter period and as the BOE staged a dramatic intervention on Wednesday to stave off an imminent crash in the gilt market.

No new leveraged loans launched in Europe in what was a choppy week for markets. Three deals did price however, although with mixed fortunes.

IT services firm Inetum was able to upsize its offering to 600 million euros from a starting range of 300 million to 400 million euros. Outsourcing provider KronosNet on the other hand, downsized its loan by 50 million euros to 400 million euros. Pricing on the deal also flexed wider. Meanwhile, eye-care firm Veonet priced a 160 million euros add-on to a larger facility it secured in April. The earlier deal had been in the market in February, but syndication was paused after Russia’s invasion of Ukraine.

The surge in global bonds after the BOE’s bond-buying program extended to Asia, with spreads on dollar notes tightening sharply. Bond issuance remained relatively subdued amid the volatility, with South Korea’s Kepco, Japan’s Komatsu and China’s Tongling State-Owned Capital marketing dollar bonds after multiple blank trading sessions earlier in the week.

— With assistance from Gowri Gurumurthy, Natalie Harrison, Ronan Martin, Colin Keatinge, Adeola Eribake, Malavika Kaur Makol and Chris DeReza

The Citrix Turning Point in Markets: Q&A

The Citrix debt sale has made it harder for banks to sell buyout bonds and loans to investors, said Michael Moore, managing director of capital markets at Union Square Advisors, a technology-focused investment bank that advises on transactions including acquisitions and capital raises.

Moore previously was a director in the leveraged finance group at Citigroup Inc. He spoke to Bloomberg’s Jill Shah in a series of interviews ended Sept. 26. Comments have been edited and condensed.

Where does the syndicated market stand after the Citrix deal?

The tone has shifted. Last week, I was cautiously optimistic. On the syndicated market, we’re now squarely in the cautious camp. Opportunistic transactions now are sidelined. A lot of people were hopeful that they could come forward with refinancing trades. That Citrix clearing and getting done well would pave the way for some stability. Clearly, that hasn’t happened.

It’s shifted the focus now back to the banks. How are they going to manage their positions? How are they going to dribble out these remaining commitments with Tenneco and Nielsen being at the top of the list? We’ll probably see some of these get restructured.

The prospect of selling them off quickly has gone away, putting pressure back on banks from an underwriting capacity and putting them out of play in the near term for incremental capital commitments.

What signs will convince banks they can sell again?

Credit markets do take their cues from the equity markets. First and foremost, what you’d hope to see is some stability in the equity markets, which obviously, we don’t have now. Even if it’s not necessarily stability, we hope to see at least trading in a much more narrow band, not these wild swings that we saw last week.

Then, you’ll hopefully start to see some stability in secondary price levels. Banks will start to bring forward the most senior tranches of those deals to the market to test the waters. And the entire market will look to say, okay, how does that deal get done? This is all save any other exogenous risks out there. The litany of things we’re watching continues to grow, particularly as you look at all the geopolitical things going on out there.

How are you advising borrowers in the technology space as valuations have come down and cost of capital has gone up?

On the credit story front, making sure they’re telling a competitive, compelling story and are buttoned up on diligence. We’re also very focused on making sure borrowers are going out to the right set of people. There tends to be, particularly in private credit, an inertia. They’ve got relationships with the top five or 10 accounts they tend to call on. Given the current backdrop, that doesn’t necessarily mean that’s the right set of investors to target because things change.

If you’ve only lined up two or three potential parties at the table to evaluate that capital, you may be left at the altar without a solution. More eyeballs on the transaction is a playbook we’ve been utilizing a lot with sponsors.

How has the private credit lending appetite changed?

With the syndicated market still very much challenged, direct lenders can step in and fill the gap. Still, accounts are certainly being more discerning. Gone are the days where you could just go to one or two accounts and speak for an entire several $100 million deal.

Leverage is coming into question. Accounts may be requiring more equity into it any given trade, which sponsors will do if and when they have to, if they’ve got good conviction on the asset, and it makes economic sense to put more equity into a deal to get it done.

Pricing is the other lever, just requiring more yield to compensate. The last is structure. Covenant packages are tighter. People will be more thoughtful about protecting themselves in the document to ensure that what they’re lending against doesn’t have any significant areas of potential credit leakage.

Investment-Grade Ratings, Junk Bond Yields

By Olivia Raimonde

Yields on blue-chip corporate debt have jumped high enough to attract some unlikely buyers: junk-bond investors.

The average yield on the lowest-rated tier of investment-grade bonds has hovered around 6% this week, the highest since 2009, when companies were recovering from the financial crisis. That’s what the best quality junk borrowers were paying as recently as August, but investment grade has much less credit risk.

“High-yield investors should extend into investment grade as much as their mandates allow,” wrote Oleg Melentyev and Eric Yu, strategists at Bank of America, in a note on late last week. “A 5%-7% yield in credits largely agnostic to recessionary outcomes is not often seen.”

High-yield money managers’ investment policies typically allow them to hold other kinds of debt. Oaktree Capital Management’s Danielle Poli has been buying more investment-grade securities given better valuations.

“For a 5% yield with very safe underlying company fundamentals, it’s a good place to hold cash in our portfolio until we await better opportunities,” said Poli, co-portfolio manager for Oaktree Capital Diversified Income Fund, in an interview earlier this month.

One reason yields have jumped on BBB rated bonds is that investors are worried about them being cut to junk, which typically results in a steep drop in price, said Bill Zox, a high-yield portfolio manager at Brandywine Global Investment Management.

“Dedicated investment-grade managers are staying away from BBBs,” Zox said. “That can result in low BBBs getting attractive compared to BBs.”

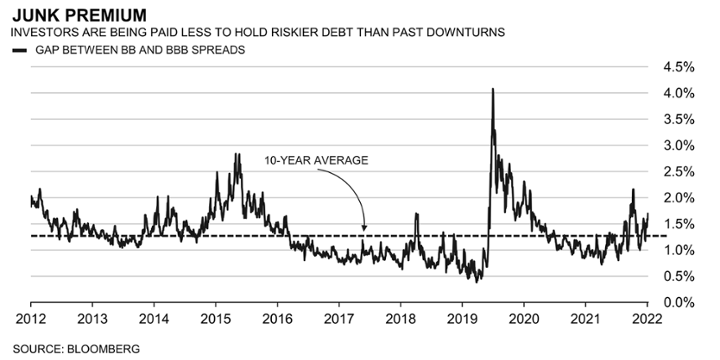

The difference between spreads on BBB and BB bonds is about 1.7 percentage points, lower than in past downturns. As a result, investors aren’t getting paid significantly more for taking extra credit risk.

“We are going into a slow-growth environment, so the premium should be larger,” Vishal Khanduja, co-head of US multi-sector fixed income at Eaton Vance. “That’s why we are preferring to own more BBBs, or investment-grade companies, versus BBs. The goal here is to be a little bit safer, a little bit more high quality.”

In the BBB market, CreditSights Inc.’s Winnie Cisar, global head of strategy, recommends debt from the likes of General Motors, HP and Warner Bros. Discovery, given spreads that are wider than debt with the same rating.

“BBB valuations, especially on a yield basis, are compelling when compared to pre-pandemic levels,” strategists led by Cisar wrote in a note dated Sept. 14.

Bank of America strategists not only recommend buying higher-quality assets as risks of a recession loom -- they also see value in purchasing bonds with higher duration.

“Our strongest conviction is in high quality, investment-grade, and longer duration segments of the market, where we think value is back in a big way,” the strategists wrote.

At current levels, BBB notes are “a rare opportunity,” the Bank of America strategists add.

To be sure, high-grade debt is hardly a slam dunk. Given its higher duration than junk, there is more interest-rate risk at a time when the Federal Reserve is hiking rates, and BBB notes have lost more than 18% this year.

But some BBB rated bonds have lower duration and higher yields than the average for high-grade. For example, a T-Mobile USA bond due in April 2030 with a 3.875% coupon yields more than 6%.

Banks are buying single-name credit default swaps on loans in their books to free up capital, often on blue-chip names like IBM and and McDonald's. Demand for that protection has driven CDS higher on those names, so an investor can sell protection on them and use that premium to buy CDS on companies that will have real problems in a recession, said Saba Capital's Boaz Weinstein in an interview with Bloomberg Markets magazine, adding, "that's what I'm spending most of my time on."

Collateralized loan obligation prices are dropping as Wall Street banks retreat from buying the securities, pressured by regulators and buyout debt losses. Dwindling demand is likely to dent issuance of CLOs, which buy leveraged loans and repackage them into bonds. US issuance is down over 20% so far in 2022 at about $100 billion, according to Bloomberg data, and JPMorgan Chase & Co. forecasts a 40% full-year slump.

A wave of downgrades is coming for the US investment-grade corporate bond market as slower growth and tighter financial conditions start catching up to companies, according to strategists at Barclays. Companies are facing margin pressure thanks to high inventories, supply chain issues, and a strong dollar. Barclays expects the average monthly volume of downgrades to increase to $180 billion of bonds over the next half year. The current monthly average is closer to $40 billion. Barclays’s forecast is based on a model that considers the historical relationships between downgrades and macro and credit market factors including the US manufacturing Purchasing Managers’ Index, the Federal Reserve’s Senior Loan Officer Opinion Survey and high-grade corporate bond spreads.

Higher rates are rapidly boosting US corporate pension plans, which are expected to sell equities and pump $550 billion into the beleaguered US bond market. Analysts expect a major shift into top-rated corporate bonds to get started soon as pensions hedge liabilities by buying relatively safe debt. The funded ratio for the 100 largest corporate defined-benefit pension plans increased to 106.4% in August, according to data from Milliman. Until this year, they had been under-funded on average since before the global financial crisis. A July analysis from BofA and BCG Pension Risk Consultants. anticipates that demand for long-term fixed income -- particularly corporates -- from pension derisking will be about $550 billion over the next five years. But that’s the base case -- if rates continue to rise and plan funded statuses go even higher, a bigger shift to fixed income could occur, creating up to $2.3 trillion of demand for longer-duration bonds over the period, the analysts found.

Big currency moves are forcing foreign buyers of US corporate debt to sell in order to hedge the risk, said Bradley Rogoff, head of FICC research at Barclays. Foreign investors faced with negative-yielding debt were lured into dollar debt early this year because “that was the place you could get yield,” Rogoff said on Bloomberg Surveillance. Hedging currency exposure is now getting too expensive for many of them.

JPMorgan Asset Management strongly favors investment-grade credit over high yield due to a sluggish growth outlook in the US and recession risk in Europe over the next 12 months, according to Sylvia Sheng, global multi-asset strategist. Estimates credit spreads to widen further “even if defaults remain contained” in the case that equities have yet to see their cycle lows, Sheng wrote in a report this week. US IG corporate bond spreads have widened about 66bps this year to 158bps through Sept. 28, Bloomberg-compiled data show.

CLO AAA and AA tranches were unaffected in stress-testing scenarios even as the global economic outlook continues to deteriorate, Barclays analysts Keyur Vyas and Jeff Darfus wrote in a research note late last week. CLO fundamentals are healthy, but tighter financing conditions alongside mediocre economic growth and weakening credit fundamentals warrant a resiliency check.

Investment-grade bond supply may be muted for a second straight month, as “market conditions will likely remain challenging,” according to Bank of America. October high-grade supply could reach $60 billion to $80 billion, well below the month’s $106 billion five-year average, strategists led by Yuri Seliger wrote in note this week.

Some green bonds issued by US utilities are trading at expensive levels relative to conventional bonds from the same issuers. This probably means investors would be better off buying the regular bonds from the same borrowers. Christopher Ratti, senior ESG analyst at Bloomberg Intelligence, said seven green bonds that he reviewed were trading at an “outsize” premium based on their duration, coupon type and payment rank.

Credit Suisse Group’s global head of credit products Daniel McCarthy has left the Swiss lender to pursue other opportunities, according to a memo seen by Bloomberg. Joel S. Kent is set to replace McCarthy, according to a separate memo sent by Jay Kim, global head of fixed-income credit products, and reviewed by Bloomberg.

Bank of America promoted managing director David Scott to head of global debt advisory. Scott, who’s based in Charlotte, North Carolina, will report to Sandeep Chawla and Jon Klein, co-heads of global investment-grade capital markets, they wrote in a memo with Elif Bilgi Zapparoli and Sarang Gadkari, the bank’s co-heads of global capital markets. Scott’s appointment follows the death in August of Andrew C. Karp, who was vice chairman of debt capital markets and global head of debt advisory.

Royal Bank of Canada’s capital markets unit has named Ram Amarnath, Graham Tufts and Harold Varah as global co-heads of its financial sponsors group, according to an internal memo seen by Bloomberg. In addition to their expanded responsibilities, Varah will remain co-head of the US financial sponsors group, Tufts will maintain his regional responsibilities in Europe and Amarnath will continue to provide senior coverage across the bank’s Canadian clients. A spokesperson for RBC confirmed the contents of the memo.

B. Riley Financial Inc. has hired Marc Walters most recently from Fifth Third Bank and Craig Zando from RBC Capital Markets to its growing fixed-income team. Walters will be focused on investment-grade sales while Zando will be responsible for high-yield sales, according to a person familiar with the matter. Both started this week and will report to Tim Sullivan, head of fixed income at the firm.

Erica Frontiero, chief operating officer of global capital markets at The Carlyle Group, left weeks ago to pursue other interests. She joined Carlyle in 2016 as the head of capital markets for private credit. She didn't immediately respond to request for comment.

Anarchy in the UK Credit Markets

By Bruce Douglas and Giulia Morpurgo

It’s a sign of just how troubled a market is when the price of roughly a third of the safest sterling corporate bonds drops into distressed territory, compared to just one at the end of last year.

Bloomberg’s index of investment-grade sterling company bonds had 339 securities quoted at below 80 pence on the pound as of Sept. 28, a threshold generally used to indicate distressed territory. Over half the index consists of UK companies, including those of pharmaceutical firm GlaxoSmithKline, British Land Company and British American Tobacco, some of which are quoted below the threshold.

Most of the jump in the number of distressed bonds happened on Sept. 23 and 26, triggered by the government’s plan to fund the nation’s biggest tax cuts in 50 years through more borrowing. While the UK credit market was already having a difficult year, the resulting selloff in the pound and government debt, put sterling notes at the center of the world’s worst bond selloff in decades. At the peak, there were 380 securities in the index trading below 80 pence.

Then the Bank of England announced it was intervening, buying long-dated gilts to stabilize debt markets. Credit markets broadly rallied, but 339 bonds remained below 80 pence. It’s worth noting that not a single bond’s spread was above 1,000 basis points, another measure of whether bonds are distressed.

Returns on the index for 2022 are down almost 25%, more than double the annual drop for 2008, the index’s worst year on record.

“We’re shifting from a near-term recession scenario to potentially a more sustained stagflationary backdrop and a more aggressive central bank, neither of which is likely to provide much comfort or confidence to investors,” wrote JPMorgan Chase strategists including Matthew Bailey in a note advising investors to steer clear of sterling credit. “We’ve been looking for sterling to underperform euros over the second half of the year since our mid-year outlook, and this continues to be our view.”

— With assistance from Tasos Vossos.

Editor Responsible: Dan Wilchins dwilchins@bloomberg.net

Data: Michael Gambale mgambale2@bloomberg.net

Subscribe at BRIEF<GO>

Subscribe at BRIEF<GO>